Every January, I clean up my financial closet. I review the past year, plan for the upcoming year, and take stock of progress toward my financial goals. While this blog isn’t a personal finance blog, it wouldn’t be fair to the reader to understand my evolving roadmap to a world of independent IR practice without understanding how personal finances influence our professional lives.

Early financial independence became essential to me when I was in my first job and came to the harsh realization that my local IR job market was not ready to accommodate someone interested in developing a longitudinal clinical practice. I realized I had to create something for myself to obtain professional satisfaction in this field. Unfortunately, doing so would mean living with some degree of financial uncertainty and forgoing a very high opportunity cost in traditional hospital-based practices. I’m still angry about the truth I have learned and wish I knew the people who I now surround myself with much earlier. Thankfully I have made some significant moves to improve my life in medicine as I continue along a path of independent IR practice.

Even with a life now that is significantly better than it was several years ago, I do not take any solace in a secure financial future in this profession. Neither should you. If you enjoy practicing medicine, you must accept the harsh reality that reimbursement will likely worsen significantly during your career. That’s not to say that you cannot have a comfortable living as a physician in the current fee-for-service environment. Still, there are significant headwinds and a future where financial security through medical practice isn’t as inevitable as it once was. Please see The Four Routes to Profitability in IR: The Plight of the IR Opportunist for further details regarding the dirty financial truth very few want to discuss.

Regardless of your opinions about IR Opportunists, suppose you are interested in a future independent IR practice. In that case, you need to take your finances seriously since your ability to create a practice cannot be divorced from your personal finances. Too often, our financial situations adversely affect our ability to be entrepreneurial, particularly for us generally risk-averse physicians with a relatively high opportunity cost in a traditional IR/DR practice. There tends to be an attrition of ambitious IR physicians within 5-10 years post training in which they succumb to the reality of the market, and that fire in their belly which was once present seems to fade out. I know of too many people who feel trapped by golden handcuffs and are afraid to try something different. I’ve received terrible job offers, with the offering party believing they have financial leverage, given my age and perceived financial circumstances. The generalized perception of young IRs is that we have a huge loan burden, expect a large salary, and will do what is necessary to make ends meet, even if this means signing our lives away to work in a less-than-ideal situation.

Financial freedom has allowed me to pursue an unconventional path, speak my mind to advocate for others, and take risks that many physicians of my era are afraid to take. What makes my story interesting is the fact that it is incredibly boring. Anyone with the appropriate mindset can do what I did.

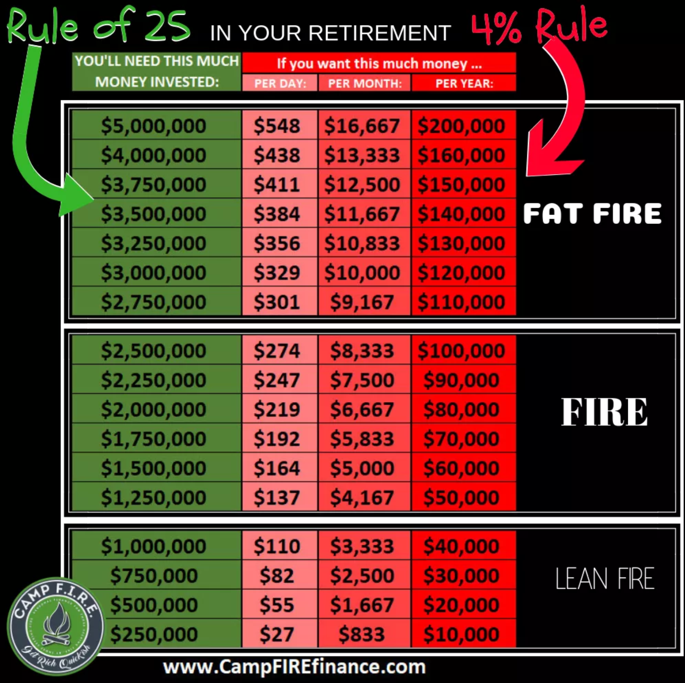

Understand what it means to be financially independent

Financial independence is not needing a job to cover one’s living expenses. Those in the “financial independence retire early” or “FIRE” community designate several levels of financial independence. See this chart for more details:

Simply put, one can safely live on 4% of their invested net worth annually and have a statistically low probability of running out of money before they die. This analysis derives from a study from Trinity University, informally known as the “Trinity Study.” While the original study shows the safety of a 4% withdrawal rate when simulated over 30 years, there have been variations of this model run for various portfolio allocations and for other time frames. For example, a stock-heavy portfolio at a 3.5% withdrawal rate can have close to a 100% probability of success over a 50-year time horizon. Armed with this knowledge, it’s generally pretty easy to figure out what kind of nest egg one will need to retire early if that is one’s goal.

It is essential to remember that this analysis assumes investment in an S&P 500 index fund. Your required nest egg will vary if investing in other asset classes, such as real estate. Everything ultimately comes down to your portfolio’s yield over time.

So how does one achieve financial freedom as fast as possible?

Have a Plan and a Why:

The most important thing people need to do is work backward from a goal to accomplish it. There is no better way to do this than to write out your plan and the steps you will take to achieve it. If you need help writing yours, copy the one from the White Coat Investor and make modifications necessary to fit your goals and personal circumstances. You will likely fail without a clear plan and a reason for that plan.

My why is simple: I want to be a practice owner and position myself to advocate for lasting change for our profession. I do not want financial considerations (golden handcuffs/large opportunity costs) to get in the way of achieving my goals. Early financial independence allows me that flexibility.

My plan is also straightforward, primarily based on the WCI plan with a 50/50 index fund and alternative investment allocation. I’ll share this in a future Newsletter (please subscribe).

Save a lot.

There isn’t any secret to financial independence. As high-income professionals, we have the luxury of making a significant amount of money relative to the general population. Sure, I get fired up about various inequities in our profession, which you hear about on this blog and can likely ascertain from the content I promote on my social media accounts, but we cannot deny that we make a lot of money.

You can accumulate wealth quickly if you maintain your budget from residency as an attending interventional radiologist for a short period after training, you can accumulate wealth quickly.

As a radiology resident in California, I made $75,000. After taxes, this amounted to about $50,000. I maintained a $50,000 budget for training and gave myself a 10% raise for every marginal $100,000 I earned as an attending. This has allowed me to maintain a savings rate above 60% of gross income.

Play Offense and Maximize Your Revenue Potential

The average interventional radiologist makes $550,000. I started my career making less than half of that, eventually coming to my senses and realizing that I should not accept such unfavorable terms. I have since gotten my act together by putting myself in a position to earn significantly more. For me, this has included leaving traditional employment, refusing promises of “partnership,” and pursuing pure independent contracting. At first, this was through an “eat what you kill model” with minority ownership in an OBL I helped to build. For the last 18 months, I have been an independent contractor for hospitals and outpatient facilities to maximize income and learn from mentors before embarking on a practice development journey. Being an independent contractor has allowed me the flexibility to choose who I want to work with and for how much. The subsequent significant increase in revenue has turbocharged my wealth-building.

Diversify Your Streams of Income

An independent contractor cannot rely on a single client to provide ongoing work opportunities. I have been fortunate to have established meaningful relationships with several practice owners, resulting in some semblance of stability in the near to intermediate term, but work is never guaranteed. While this is especially true in the locums world, this also applies to permanent employment. You cannot accept that your job is guaranteed.

As such, I have diversified my income stream to include multiple clinical and non-clinical sources. Check out this post for more information. For the typical physician, non-clinical income sources can include investment income from their stock portfolio, real-estate holdings, or other income-producing assets such as small business ownership. This is how real wealth is made and compounded over time. In order to create financial freedom, it is essential to take your money made in medicine and invest aggressively into other non-correlated income-producing assets. This message is even more true for those like me who seek an entrepreneurial path and hope to create opportunities for other IRs.

Learn to Hit Singles Consistently. Home Runs Are Not Necessary.

Financial literacy among physicians could be much better. Unfortunately, many physicians are suckered by financial advisors and find themselves off-loading their finances to some third party who charges significant fees for the promise of potentially beating the market. The sad truth is that very few people can beat the market, so it is in most investors’ best interest to invest in low-cost index funds to obtain market returns.

A book that has changed my mindset about investing is The Simple Path To Wealth by JL Collins. This book is kind of like The Bible of FIRE movement aficionados. The entire premise is to invest in low-cost index funds to obtain market returns over a long time horizon. Collins promotes a message of “time in the market” to trump any efforts of “timing the markets.”

If one can achieve a 6-10% return on their investments over 30+ years, that individual will be happy with their overall portfolio growth. Investing does not require any significant nuances other than finding low-cost index funds and selecting an asset allocation of stocks and bonds that will allow you to sleep well at night. Stocks will allow for the highest returns over time, but bonds will help smooth the ride. Please read the Collins book for more elaboration on this concept. If you can learn to do a TIPS, you likely have enough neurons to learn this stuff.

Learn to Play Defense: Keep Your Expenses Under Control

I have many friends who have grown too comfortable attending IR lifestyles. The problem with lifestyle inflation is once you experience that sweet taste of the good life, it takes a lot of work to return to living like a resident. Here are common scenarios that can result in lifestyle inflation:

- Choosing to live in a high-cost-of-living market.

- Purchasing a “doctor home” immediately out of training.

- Buying high-end luxury vehicles.

- Taking multiple five-figure plus international trips annually.

- Underestimating the cost of kids

Before this blog gets canceled, let me explain.

Life is full of choices. I’m a firm believer in the fact that we can afford anything, but we cannot afford everything. What we spend our hard-earned dollars on is a function of what we value.

Where we choose to live and work is a choice. It may not seem like it to some due to spousal or family considerations, but it is genuinely a choice at the end of the day. If your future requires you to live in Manhattan or the Bay Area (both places I’m very familiar with), then you have to budget appropriately for those locations. It won’t be fun, but that’s the price you pay. Unlike most other industries, high-cost-of-living markets tend to have the lowest physician pay.

Regarding kids, I’m not saying don’t have kids. I’m just saying they can be expensive, and you have to consider that. Childcare isn’t cheap, but it is necessary for many scenarios where there may not be a parent or other family member to take care of your kids while you are working. Sadly, given our training, many people who wish to have families will do so in the years when it is most prudent to save and invest aggressively.

Concerning home ownership, I generally think it’s a bad idea to buy a home immediately when taking your first job. Many of us change jobs, and you never know how things will go. Homeownership can be a great financial tool, but only in a growing market where you will be for at least five years at a minimum, as transaction costs can easily wipe out any appreciation.

Regarding luxury items such as expensive cars, fancy vacations, and weekend getaways to famous destinations, there is nothing wrong with indulging in things that genuinely bring you joy. But you cannot live like a rockstar when you simply aren’t one. I’m sorry, but the American physician is not a rockstar. Maybe once upon a time, but not in 2023. We’re high-end wage workers trading time for money. High income does not translate to wealth without discipline.

What we value differs among us, and personal finance is personal. My decisions may not be your decisions, and that’s fine. But if you want to be financially free and put yourself in a position where you don’t need a job, then you will need to make your own hard choices to get to that point.

I spent the first three years post-training tracking my spending using the YNAB app. I found this very helpful because it gave me data about my spending habits and allowed me to fine-tune my budget over time, focusing on things that brought me value. I don’t necessarily think everyone needs to pay for fancy software to track their spending, but I do believe that most physicians should budget at some point to get an idea of their habits and collect data. Without tracking this stuff, it’s hard to get a sense of where your money is going.

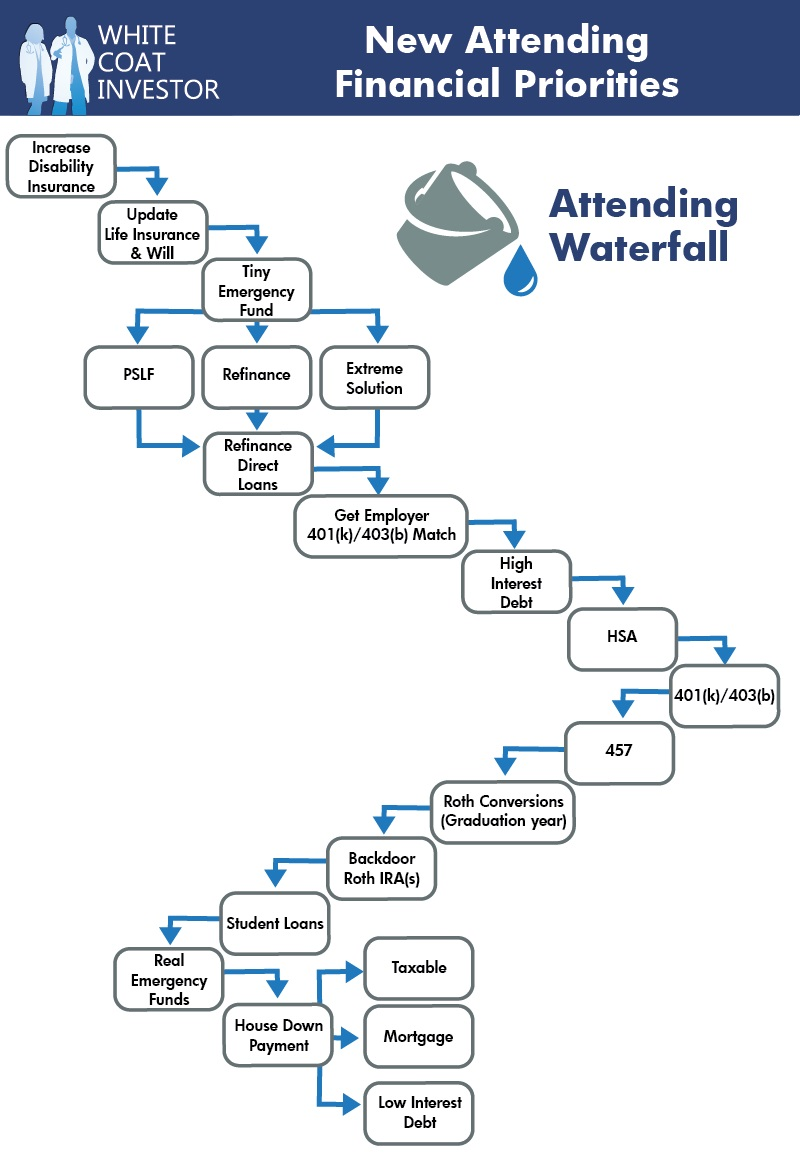

Fill Your Buckets

The “Attending Waterfall” structure from the White Coat Investor is an excellent overview of how one should allocate their money when the big checks start coming in. This is what I did, which you may find helpful or not helpful, but it seems to be working out just fine for me:

- Obtaining Disability Insurance as a Resident

- Pay Off Student Loans Immediately

- Maximizing Pre-Tax Retirement Contributions

- Backdoor Roth IRA Contributions Annually

- Automatically deferring a large proportion of my post-tax income to investments.

The traditional concept of retirement via index fund investing focuses on taking a “safe withdrawal” of invested capital which is very tax-efficient and generally assumes you will reliably earn income over several decades. However, suppose you find yourself in a position, as I found myself, where maybe you don’t want to have a “regular job.” You sense some doubt or uncertainty about a conventional path. In that case, it becomes imperative that you find ways to replace your income to support your lifestyle as you embark on an entrepreneurial path that will inevitably have peaks and troughs.

Accelerate The Development of “Passive Income”

I’ve shifted my philosophy away from obtaining a target “nest egg” to one where I am focused on developing “cash flow” from my investments. To do this, I have had to force myself to learn skills outside of traditional personal finance mantras summarized above, which are a dime a dozen these days with the proliferation of FIRE blogs and physician finance content. Line Monkey MD is not another FIRE blog; the average reader here likely has an IQ that exceeds mine. So as I graduate from undergrad level finance content, I will be happy to bring you post-grad content as I live it.

To replace my living expenses as soon as possible, I had to learn to invest beyond index funds into alternative investments such as real estate and small businesses. While an index-fund-only approach is appropriate for most individuals, index funds are not meant to be tapped into for decades into the future. For me, allocating a proportion of my overall portfolio to alternative assets has been crucial in developing a sound long-term strategy and sufficient near-term tax-advantaged cash flow to give myself a buffer for when I take the leap into making a significant practice investment. I will dissect the strategies I have been employing in a series of future posts. Stay tuned.

Making Mistakes

I think too often, discussions about personal finance can seem very judgemental, and that’s often reflected in the tone of some of the people who teach this content. We all must have humility and accept that we are imperfect beings. Mistakes are inevitable.

I’m more than happy to share some of the mistakes I’ve made regarding money so you can avoid them. Here goes:

- Agreed to a job with a significant vesting period for pre-tax retirement contributions.

Long-time readers know that my first job was a terrible one for me. I essentially picked it out of convenience and a false perception that I could change a culture that didn’t want to be changed. Unfortunately, like many private practice jobs, one of the traps with this job is a pre-tax retirement account with a vesting period. In particular, my job would vest at 20% yearly for five years. I left after 20 months, meaning that only 20% of the portfolio value would be mine. The group invested nearly $80,000 over those two years, and the portfolio is now worth over $120,000 due to the insane bull market at that time. That’s a multiple six-figure mistake 34 years from now when I have to start withdrawing from that account.

Ultimately, vesting periods are like traps. I’d be very cautious about these types of plans which are unfortunately common. I’d also be cautious of retirement plans that don’t allow you to maximize your pre-tax contributions. Please educate yourself and inquire about your employer’s retirement plans. Ultimately, nothing would keep me in a terrible situation, and moving on was the right move despite the financial consequences.

- Not negotiating tail insurance with my first employer.

This was also a very costly mistake on my end. A $25,000 one. I’m lucky because, in many larger, more litigious markets, this could easily be a six-figure mistake. Writing a large check when you’re leaving a job, already feeling like total crap and uncertain about your future, is truly an insult to injury. Try to avoid it.

- Not fully understanding practice valuation when entering into an OBL partnership.

New medical practices are generally valued at 2-3x their earnings before interest, taxes, depreciation, and amortization (EBITDA). When selling out of a profitable practice, one should leave with more money than before they started there. In my contract was a clause that devalued my shares for every year up until three years into the practice-functionally no different than the pre-tax retirement account contribution vesting period I described for my first job. Having left 18 months into starting the practice, I was set to go with less than half of my upfront capital despite it being a highly profitable practice. It took me an expensive lawyer (sadly, the same expensive lawyer who had reviewed the contract in the first place) to help get my invested capital back. As much as I can moan and complain about this, I have no one else to blame but myself.

- Failure to establish a professional LLC in a timely fashion.

For the tax year 2021, I failed to establish an LLC promptly. As a very high-income year, it would have been beneficial to have established an LLC so I could file as an S-corp. That move would have saved me over $20,000. Please read this older post for more details. If you think you will make over $400,000 yearly in 1099 income, please do so with an LLC structure.

Celebrate Your Wins and Create a Better Future

Despite all these mistakes, I have reached a level of financial freedom where I no longer fear “not having a job.” I have also created a mechanism for growing my wealth significantly over time. We all have different circumstances. Perhaps some of us are more privileged going into this than others. Maybe it’ll take you more time, given your circumstances and expenses. Maybe it’ll take you less time (hopefully). The point of this post isn’t to beat my chest and tell you how great I am. It’s to show you that early financial independence is possible and that we can put ourselves in positions to excel financially. Ultimately, establishing a financial game plan is essential to pursuing an unconventional path in medicine. Given that we are a field that is evolving rapidly to a clinical specialty, those who will succeed will put themselves in a position to create meaningful opportunities for others. To do this, we simply have to say no to opportunity costs which are pretty high but do nothing to advance our field, particularly within the world of private practice. Poor personal financial situations often prevent even the best physicians and potential entrepreneurs from reaching their full potential.

I am blessed to know that I do not have to take a job because of some need to make money. Financial freedom has allowed me to take the scenic road-one that has been incredibly rewarding. There is no amount of money I would trade for the experiences and lessons I have learned to this point. I do not want to be some Zebra. I want everyone to experience what I have. The more of us who can do hard things, the sooner our field will genuinely advance. This post may be eye-opening for some of you. Some of you are savvier and think I could do things even better. Either way, please comment below and leave your thoughts.

Resources For The Interested Reader

Here are the best resources for readers interested in learning more:

The best financial resource on the internet is the Bogleheads forum:

https://www.bogleheads.org/forum/index.php.

I highly recommend that every reader check out the White Coat Investor. They have now gotten big and have all sorts of affiliate programs and things they sell. The truth is everything you need to know is on the blog and is free. Read through the posts and take notes.

https://www.whitecoatinvestor.com

For those interested in learning more about real estate, there is no better resource than Bigger Pockets. I have learned so much by reading the website and listening to their podcasts. I think of all those hours waiting for hospital transport, lamenting my existence…

Your candid sharing of personal experiences and lessons learned is both refreshing and invaluable. It’s inspiring to see how you’ve navigated the challenges of pursuing an independent IR practice while maintaining a strong focus on financial independence.

Thanks for the kind words and for checking out the blog.

I found the tips on creating financial security really helpful! It’s great to see practical advice that can make a difference in people’s lives. Looking forward to implementing some of these strategies!

Thank you for educating us. Being wise in spending and saving money is crucial to being financially secure when retirement comes.